The BCCL empire—towering over the competition

BCCL has achieved this scale mainly through diversification into a variety of non-print media and ploughing its surplus cash into many venture-fund like investment bets.

The Hoot’s ANALYST AT LARGE dissects the Times Group’s financials

Bennett, Coleman & Company Ltd. (BCCL), India’s largest media conglomerate, has in recent years acquired as much of a reputation for its money management skills as for running a successful media empire.

BCCL’s consolidated financial statements show the extent to which this sprawling empire towers over its rivals in both print and electronic media. It has achieved this scale mainly through diversification into a variety of non-print media and ploughing its surplus cash into many venture-fund like investment bets.

The company is yet to file its financials for FY17 with the MCA, and its latest available filings are for the FY16. Consolidated numbers for FY16 showed BCCL dwarfing its less-diversified media competitors both on revenues and profits.

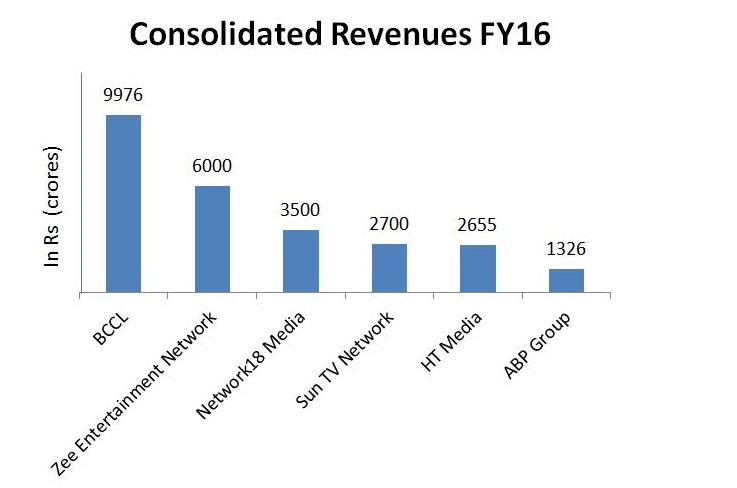

BCCL on a consolidated basis reported total revenues of Rs 9976 crore from print, television, radio and other activities. This was more than 3 times the consolidated revenues of Rs 2655 crore earned by HT Media and 7 times larger than the ABP Group (Rs 1326 crore) for the same year. Pitting the BCCL group against electronic media competitors shows that its revenues were 66 per cent higher than the Rs 6000 crore earned by Zee Entertainment Network, nearly three times the revenues of Network18 Media and Investments (Rs 3400 crore) and over 3 times the topline of Sun TV Network (Rs 2700 crore) for the same year.

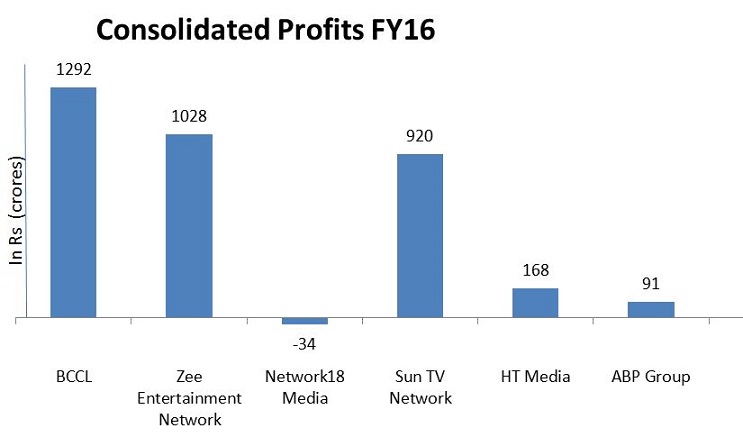

At Rs 1292 crore, BCCL’s consolidated profits were 25 per cent higher than the consolidated net profits of Zee Entertainment (Rs 1028 crore), 40 per cent higher than that of Sun TV Network (Rs 920 crore). Network18 Media reported a net loss of Rs 34 crore. BCCL’s profits also dwarfed print media rivals at over 7 times the net profits (Rs 168 crore) for HT Media (consolidated) and 14 times the after tax profits (Rs 91 crore) for the ABP group.

BCCL’s EBIDTA (Earnings Before Interest, Taxes, Depreciation and Amortization) margins are significantly superior to print media rivals, but fall short of the margins reported by its electronic media competitors. In FY16, BCCL’s consolidated EBIDTA, at Rs 2374 crore resulted in an EBIDTA margin of 23.7 per cent. The number was at similar levels the previous year. This substantially beat print rivals such as HT Media and the ABP group (they managed 15-17 per cent), but lagged behind Zee Entertainment (31 per cent) and Sun TV Network (75 per cent). Minuscule borrowings meant that BCCL got to retain a margin of about 13 per cent at the net profit level.

Many strings to the bow

Though BCCL has a significant presence across the print, television, digital and radio segments, it is hard to home in on the contributions that each of these diverse media businesses make to the aggregate numbers. This is because, unlike HT Media, BCCL in its consolidated financial statements does not provide a segment-wise breakup of its revenues or profits.

So its segment-wise financials only reveal the bare detail that ‘print media’ chipped in with revenues of Rs 6595 crore in FY16, which is 68 per cent of BCCL’s topline, earning a profit before tax of Rs 1415 crore. Another broad-brush segment termed as ‘Others’ (television, radio, internet, movies, insurance etc) accounted for Rs 3175 crore (32 per cent) of revenues and reported a loss of Rs 266 crore at the operating level.

"Unlike HT Media, BCCL in its consolidated financial statements does not provide a segment-wise breakup of its revenues or profits"

While the television business was earlier housed in subsidiaries - Times Global Broadcasting and Zoom Entertainment Network - in recent years the group seems to have transferred its flagship channels to the parent company through schemes of arrangement. The FY16 filings mention the transfer of Times Now to the parent company. It rationalized that the restructuring would help BCCL ‘share content and infrastructure between its different media offerings, and sell advertisements as a bouquet’. While the ad revenues from the television channels are likely tucked away in the Rs 6436 crore in advertising revenues reported in the consolidated financials in FY16, the group earned Rs 156 crore from TV distribution revenues, the number seeing a significant jump from Rs 63 crore the previous year.

Income from investment activities added Rs 859 crore to the operating profits of Rs 1149 crore derived from two core businesses, effectively chipping in with 43 per cent of BCCL’s pre-tax profits for the year. After shelling out taxes of Rs 696 crore, BCCL clocked a net profit of Rs 1292 crore.

"Income from investment activities added Rs 859 crore to the operating profits of Rs 1149 crore derived from two core businesses"

BCCL’s consolidated profit and loss statement for FY16 offers three key takeaways.

One, BCCL as a group is far more reliant on advertising revenues than subscription revenues for its sustenance. In FY16, advertising revenues, at Rs 6436 crore brought in nearly two-thirds of the group topline. This includes ad revenues from all the media businesses- print, television, radio and internet.

Subscription revenues generated by its media content (both print and electronic) are a relatively minor contributor to the BCCL topline. The notes to the profit &loss account reveal that the sale of publications (magazine/newspaper sales) contributed just a 7 per cent sliver (Rs 692 crore) of its total revenues in FY16, while TV distribution revenue was even smaller at Rs 156 crore. This revenue mix appears to be quite in keeping with the Group’s strategy of aggressively pricing its media offerings at low levels, with a view to maximizing either viewership or readership. Once the publication or channel garners sufficient eyeballs and is able to wean away market share from competitors, BCCL proceeds to monetize this through high advertising yields.

To be fair, aggressive pricing strategies apart, the Times group has also displayed far greater marketing savvy than its competitors in building up a readership base through brand-building investments, high-profile awards and events, and below-the-line promotional activities.

Two, BCCL’s non-media businesses make quite a sizeable revenue contribution. In FY16, for instance, the group earned as much as Rs 547 crore from ‘sale of traded products’ (the nature of these products is unknown but could represent retailing activities), Rs 333 crore from e-commerce, Rs 95 crore from sponsorships and Rs 41 crore from education services. The insurance joint venture chipped in with Rs 157 crore too.

Three, a really big buffer to BCCL’s finances comes from its investment book – part of which arises from its ‘brand capital’ business. Also known in the trade as the ad-for-equity business, BCCL sells advertising space across its numerous media outlets to business houses, which they pay for in kind - by way of equity, debentures, preference shares, warrants or even immovable property.

Churning this ‘portfolio’ of investments each year and the interest and dividend streams from it, have accounted for large chunks of BCCL’s revenues and profits over the years.

"BCCL’s non-media businesses make quite a sizeable revenue contribution"

The importance of investment activities to its finances become clear from a breakdown of BCCL’s consolidated profit and loss statement. In FY16, BCCL’s investment income from sale of investments, interest, dividends amounted to as much as Rs 980 crore and added more to the topline than the sale of newspapers (Rs 692 crore).

While investment activities add financial heft to BCCL and give it surplus cash to play around with, the profits from this source have been erratic as the bulk of this investment income represents capital gains on selling shares and securities. While BCCL made Rs 748 crore from sale of investments in FY16, in FY15 it earned just Rs 104 crore.

However, BCCL’s investment portfolio certainly gives it the flexibility to cash in on either short term or long-term investments to bolster its finances, in an indifferent year for its media business.

How subsidiaries fared

BCCL conducts its sprawling business through dozens of Octopus-like arms. Its consolidated balance sheet for FY16 aggregated the numbers from 48 subsidiaries (either wholly owned or majority owned), one joint venture (Aegon Life Insurance) and 15 associate companies where BCCL holds a minority or strategic equity stake of 50 per cent or less. Of these though, Times Internet (which houses all the digital news properties of BCCL) and Entertainment Network (which houses the Radio Mirchi brand) are the material ones from a revenue perspective. Fourteen of the 48 subsidiaries were profitable, while the rest either notched up zero profits or were in the red in FY16.

Digital: The subsidiary Times Internet Ltd, which houses the widely-followed digital news portals, is among BCCL’s most successful media-related forays. The subsidiary clocked revenues of Rs 938 crore and net profits of Rs 53 crore for FY16, making it by far the biggest digital business among India’s media groups. To put the numbers in perspective, HT Media reported digital revenues of Rs 151 crore in FY17. Times Internet is profitable while most other media houses’ digital forays are yet to turn around. Of course, the turnaround has required the group to sink in significant capital over the years. The subsidiary financials show assets valued at Rs 1371 crore and share capital of over Rs 1000 crore invested in Times Internet by FY16. Times Internet Inc (US) and Times Internet UK, also feature assets worth some Rs 205 crore, but report negligible numbers.

"The subsidiary Times Internet Ltd, which houses the widely-followed digital news portals, is among BCCL’s most successful media-related forays"

In its website, Times Internet claims over 232 million unique visitors a month across its properties, collectively accounting for 10.4 billion page views and 10 billion minutes spent across web and mobile devices. According to similarweb.com, an internet traffic tracker, timesofindia.com registered 31.7 million total visits via desktop and mobile devices in the last six months. Other news offerings such as economictimes.com (5.53 million visits in last 6 months) mumbaimirror, navbharattimes.indiatimes.com (9.8 million), and eisamay.indiatimes.com are popular with specific audiences.

Radio: BCCL’s radio business is housed in Entertainment Network Ltd, a publicly listed company in which BCCL owns a 71.15 per cent equity stake. ENIL has turned out to be BCCL’s most profitable subsidiary, with net profits of Rs 100 crore on a turnover of Rs 534 crore in FY16. ENIL being a listed company files its quarterly results with the stock exchanges. Filings for FY17 reveal that the company reported consolidated revenues of Rs 556 crore, operating profits of Rs 125.8 crore and net profits of Rs 55.2 crore. On a net worth of Rs 854 crore, the company borrowed Rs 123 crore from banks, to deploy in radio licences and other assets.

In FY17, while revenues were up 9.4 per cent over the previous year, net profits dropped 49 per cent due to higher costs and depreciation and amortization charges, probably arising from the new radio licences. During FY17, the Radio Mirchi brand participated in auctions and acquired licenses to operate FM radio in 21 new cities, expanding its presence from 43 to 64 cities. Going forward, the company plans to improve margins at existing stations, develop new business streams within FM radio and take the Mirchi brand to global markets.

Other subsidiaries: Apart from Times Internet and ENIL, BCCL’s other subsidiaries displayed a mixed record of profitability. Metropolitan Media Co (Rs 50 crore net profit), Bennet Institute of Higher Education (Rs 28 crore) and TIM Delhi Airport Advertising (Rs 25 crore) were among the material profit-making arms in FY16.

But the group’s non-media digital forays weren’t as lucrative from a financial perspective. MagicBricks Realty Services, with a share capital of investments of Rs 82 crore, managed Rs 125 crore in revenues, but ran up a loss of Rs 77 crore in FY16. Gamma Gaana Ltd (net loss of Rs 114 crore in FY16) and Times Centre for Learning (net loss of Rs 38 crore) were also loss-making.

Zoom Entertainment Network with a share capital of Rs 110 crore, clocked Rs 124 crore in revenue and made just Rs 8 crore in net profits last year.

Other arms that have seen high capital commitments but were loss-making are Brand Equity Treaties (Rs 201 crore share capital, Rs 12 crore losses) and Junglee Pictures (Rs 112 crore capital, Rs 9 crore loss).

Investment business

BCCL’s consolidated balance sheet also reinforces the impression that this is as much a portfolio management firm, as a media conglomerate.

True, BCCL boasts a rock-solid balance sheet. On a shareholders capital of Rs 287 crore, the company has amassed Rs 9313 crore as reserves and surpluses over the years, making for an aggregate net worth of Rs 9600 crore. Though this net worth endows it with considerable borrowing power, the company uses hardly any debt in its business. Its aggregate debt (short plus long-term) at Rs 264 crore, as of March 2016, was a minuscule 0.02 times its shareholders’ equity.

However, core business assets such as fixed assets (Rs 2819 crore), receivables (Rs 1681 crore) and inventory (Rs 525 crore), loans and advances (Rs 1067 crore) take up only about 40 per cent (total assets of Rs 15622 crore) of the BCCL balance sheet. It is the Rs 8900 crore investment book, comprised of both short term and long-term investments that makes up the bigger component of assets.

"BCCL’s consolidated balance sheet also reinforces the impression that this is as much a portfolio management firm, as a media conglomerate"

This sizeable investment portfolio is divided into short-term investments of Rs 3844 crore and long-term bets of Rs 5062 crore. Where is this mammoth portfolio invested? Examining the long-term book first, about a fourth of it, or Rs 1178 crore is invested in BCCL subsidiaries, with another big chunk of Rs 1747 crore invested in immovable properties. Apart from this, BCCL has been quite a prolific investor outside of its businesses too. The long term investment book features Rs 463 crore in equity shares and Rs 273 in equity warrants of other companies, Rs 239 crore in debentures of other companies. It also features government bonds worth Rs 502 crore, mutual fund units worth Rs 236 crore, with a nominal Rs 25 crore parked in a venture capital fund and paintings valued at Rs 2.8 crore.

While it is a prolific investor no doubt, BCCL has had mixed success with its long-term investment bets. The balance sheet reveals cumulative write-offs due to ‘diminution in value’ totting up to Rs 624 crore (about 34 per cent of cost) in BCCL’s subsidiaries.

On its other equity investments, it has taken cumulative write-offs of Rs 465 crore or about half of cost (until March 2016), with smaller haircuts on preference shares, debentures, warrants and property investments.

As of March 31 2016 though, the quoted investments showed a market value that was 27 per cent higher than book value, totalling Rs 1497 crore. The unquoted investments were valued at Rs 3883 crore.

For parking its short-term surpluses, BCCL preferred mutual funds with Rs 3278 crore invested in them in end March 2016. The ‘current’ (readily liquidatable) investment portfolio also held Rs 243 crore in shares of other companies, Rs 190 crore in debentures, Rs 42 crore in FDs, Rs 74 crore in government securities and Rs 15 crore in property.

Overall, while its non-business related investments give BCCL financial muscle, they also make for higher linkages between BCCL’s financial fortunes and the state of the stock markets. Portfolio churn, which has contributed a significant chunk to the media giant’s topline and bottomline in recent years, may yield positive results only when market conditions are favourable.

Recently assigning a high AAA rating to BCCL’s bank loan facilities, CRISIL cited BCCL’s strong market position in English newspapers, its high ad revenue yields, strong financial profile and financial flexibility owing to its cash coffers, as key pluses.

"The statutory filings do not make distinctions between BCCL’s ad-for-equity investments and investments made for business diversification"

However, it drew attention to BCCL’s subsidiaries (29 per cent of net worth) for delivering ‘muted returns’. It also flagged that 35 per cent of BCCL’s balance sheet was deployed in the ‘brand capital’ (ad-for-equity) portfolio valued at Rs 3100 crore and noted that this subjected BCCL to ‘market risks’ given the large investments in unlisted companies and property.

The statutory filings do not make distinctions between BCCL’s ad-for-equity investments and investments made for business diversification. Therefore, it is hard to gauge the performance of the controversial ad-for-equity business on a standalone basis.

Backdrop

The publisher of newspapers such as The Times of India and The Economic Times, BCCL has gone from strength to strength in the 179 years since inception. Relentless diversification and financial savvy, combined with a keen focus on the commercial aspects of the media business has ensured that BCCL has evolved into the Goliath it is today.

BCCL’s main print publications occupy pole positions in their respective markets. Audit Bureau of Circulation numbers for July-December 2016 place the flagship Times of India’s daily circulation at 31.8 lakh, making it the largest circulated English daily in India. It is also the only English newspaper to figure in the list of the top ten newspapers in India. TOI and Economic Times (which sells 3.9 lakh copies a day) both have huge leads over their nearest rivals. Traditionally strong in the Western and Northern markets, BCCL has made a push into the Southern markets in the last decade and wrested market shares from rivals.

Navbharat Times, the Hindi daily that flagged off the Group’s language foray, is now flanked by Maharashtra Times, Ei Samay, NavGujarat Samay, Telugu/Tamil/Malayalam Samayam and a clutch of tabloids – Mumbai Mirror, Kolkata Mirror, Ahmedabad Mirror, Bangalore Mirror. Also in the fold are magazines - Filmfare and Femina. The group also has presence in radio broadcasting with the popular Radio Mirchi, through a subsidiary Entertainment Network India Limited. Zoom TV (a general entertainment channel), Times Now (English news channel), Mirror Now, ET Now (business news channel), Romedy Now, Movies Now, and Movies Now Plus complete the group’s electronic media portfolio.

In its FY16 annual report, BCCL claimed that the ten-year old Times Now had a 42 per cent category viewership share in English News. ET NOW, it claimed, had a 44 per cent market share. The entertainment and Bollywood centred Zoom was relaunched during the year with a new logo and positioning line and visual identity. While Romedy Now completed two years, Movies Now and Romedy Now were launched in the high definition segment. MN+ was kicked off as a premium channel beaming Hollywood movies and Magicbricks Now, was launched to provide trade information on the property space.

BCCL was among the first movers in the digital space way back in 1999. The digital properties of the group are housed in the subsidiary Times Internet Ltd. BCCL’s digital business spans not just content (news, entertainment and sports), but also commercial portals engaged in classifieds, e-commerce and startup investments. These include gaana.com (commercial music streaming service), cricbuzz.com, male lifestyle platform mensxp.com, and zigwheels.com (auto review portal) catering to niche audiences. In the classifieds space, it runs Magicbricks, Timesjobs, and Techgig.

Ownership

All large media groups in India operate through a web of holding companies and subsidiaries. BCCL’s web is just larger and more tangled than most.

As per the consolidated financials for FY16 filed with the MCA website, the promoter holdings in BCCL are distributed between 8 private entities. These are: Bharat Nidhi Ltd (24.41%), Ashoka Viniyoga Ltd. (18.02%), Camac Commercial Co. Ltd. (13.30%), Sanmati Properties (9.75%), Arth Udyog (9.31%), PNB Finance & Industries (9.29%), Jacrandra Corporate Services (8.93%) and TM Investments Ltd. (5.96%). In all, these eight entities control 98.97% of the equity in BCCL. Members of the promoter family - Vineet Jain, Meera Jain and Samir Jain own less than 1 % each in their individual capacities.

"All large media groups in India operate through a web of holding companies and subsidiaries. BCCL’s web is just larger and more tangled than most"

But digging deeper into the eight promoter entities reveals that they in turn feature holdings in each other and as well as shareholders from the Jain family. For instance, Bharat Nidhi, the largest promoter entity in BCCL, has private companies and individuals owning a 96% stake, with its biggest shareholders being Vineet Jain, Sanmati Properties, Arth Udyog and TM Investments. Similarly, Ashoka Viniyoga’s top shareholders include Samir Jain, Camac Commercial Co. Ltd., and PNB Finance & Industries, among others. Further digging suggests that other promoter entities also feature family members or group entities as promoters.

Why do business houses go in for this onion-peel ownership structure? Well, using holding companies to route ownership stakes makes it easier for a group to reshuffle equity stakes in various businesses, exclude or add new promoters, structure compensation or receive equity infusion, one level removed from the main entity. This also brings with it less public scrutiny.

Management

BCCL is managed by Sahu Jain family members. The Jain family came into the ownership of BCCL in late 1940s. Sahu Shanti Prasad Jain, Vineet Jain's grandfather, apparently bought the firm from his father-in-law Ramakrishna Dalmia. Samir and Vineet’s mother Indu Jain is the chairperson of BCCL.

The massive expansion drive and an overhaul of BCCL’s strategic direction happened in the late 1980s when Samir Jain, Vineet's elder brother, took charge as Vice Chairman.

Known to be spiritually inclined, Samir Jain’s approach to the paper was markedly different from his father’s. He inducted marketing brains into the Group and slashed cover prices for flagship newspapers, in a move that squeezed rivals. He systematically refocused BCCL’s publications and electronic media to specifically target the youth as their audience, offer a mix of feel-good stories to connect with readers and strengthened the hands of BCCL’s ‘response’ (advertising) division. This was a very corporate and consumer-oriented approach which in the initial days ruffled quite a few feathers.

His brother Vineet took this strategy a notch higher, re-imagining the company as an advertising powerhouse, and not necessarily a content-led media empire. It is thanks to this laser focus on the commercial aspects of the business that BCCL’s investment empire today sprawls well beyond the print publications it started out with.

Disclosures in the related-party transactions section of the annual report show that Vineet Jain received Rs 63.59 crore by way of remuneration and rent from the consolidated entity in FY16 and Samir Jain received Rs 62.46 crore, while Indu Jain received Rs 15.9 crore by way of rent and remuneration. This is apart from a long list of companies and entities in which the promoters are stakeholders, which also received payments by way of related party transactions with BCCL.

The Hoot is the only not-for-profit initiative in India which does independent media monitoring.

Subscribe To The Newsletter