Network 18 Part 1--Beginning with a bang...

As part of the Hoot's focus on the financials of media companies we carry a four-part series on the trajectory of Network 18. Part 1 makes the point that as of now ordinary investors in Television Eighteen India Ltd and the subsequent CNN IBN IPO have got a raw deal on their investment. Part 2 starts with the dilution in promoters' shareholding and describes how the contours of restructuring were such that it magically transformed the minority stake into a majority. Part 3 deals with some of the biggest strategic investments made, how they fared, and how they sowed the seeds for the incumbent promoters losing control. Part 4 deals with the entry of Reliance, tied also with TV18 taking over from Reliance their stake in Eenadu TV. It then goes on to deal with the performance post-takeover.

On February 8, 2016, a year and three months ago, investors at the Bombay Stock Exchange were greeted by an announcement by Network 18 Media & Investments Limited (NMIL). The company said that Raghav Bahl, one of its directors, had resigned from the Board of Directors due to what it termed as ‘his pre-occupation’.

A similar announcement was made by the company’s operating subsidiary in the broadcast business, TV18 Broadcast Limited (TV18) on the same day. The curtains thus finally came down on the association between a media group that has had, in the last decade or so, more ups and downs than a roller coaster in an amusement park, and its founder and most visible face.

That something like this was inevitable once Bahl lost ownership control of the media group in 2014 or, as some would say in 2012 itself, is not in doubt. But given how the company began with a bang on the stock market, did it really have to end this way?

Television Eighteen India Limited‘s (TEIL) journey and the fortunes of investors who flocked to it in the early days and who kept faith with it for many years later is worth recounting.

When TEIL - which in later years morphed into two separate units, TV18 and NMIL - made a maiden offer of shares to the public back in December 1999, it received an overwhelming response. The company had, just prior to the public issue, successfully launched a television channel for providing business and financial market news.

The company, promoted by a veteran media professional Raghav Bahl and a small band of associates, priced the issue at Rs 180 a share with a premium of Rs 170 to the face value of Rs 10 per share. This was meant to raise a mere Rs 50-odd crore. But such was the hype around the issue that it had been oversubscribed 64 times when the offer closed.

On the day the company’s shares were traded on the national stock exchanges for the first time, a report in the Indian Express said that shares of the company touched a high of Rs 1,950 at the Bombay Stock Exchange before settling down at a very healthy Rs 1,667 per share by close of the day.

The appeal of business news on television

The novelty of a business news-oriented channel delivered to an audience that was accustomed to consuming such news through the print medium until then, had its allure for the investing public. Its association with CNBC, the leading business and financial news channel of the United States, only enhanced its appeal.

But more than these obvious advantages, the channel was delivering a consumer audience that was high on disposable income, a target that no prospective advertiser could afford to pass up. In short, it was a perfect match between a company and an investing public, made in IPO heaven!

But what was thought of as a compelling investment proposition at the time of the IPO, had since unravelled so thoroughly that investors can be pardoned for being befuddled. Far from appreciating in value, it has practically stagnated. To compound matters, the risk profile of the initial investment too had undergone a sea change.

Losing focus with a melange of channels

It was no longer about exposure to an enterprise broadcasting business news in the English language. In just about 10 years, shareholders traded their investment in an exclusive business news channel in the English language to a new company (TV 18 Broadcast Limited) hosting a potpourri of television channels - business news, general news and general entertainment.

It was also no longer about broadcasting in the English language but Hindi and a host of other regional languages as well. It was also simultaneously about investing in the shares of a new company (Network 18 Media Investments Limited) that boasted of stakes in a variety of non-media related digital and other businesses including making and distributing feature films! The original investors wouldn’t have minded the trade-off but for the fact that they were now considerably worse off than before.

As an illustration, the initial investment of 100 shares in TEIL which cost an investor Rs 18,000 at the time of the IPO got transformed into 280 shares in TV 18 Broadcast Limited (TV 18) and 157 shares in Network 18 Media and Investments Limited (NMIL) through a series of restructuring exercises and other corporate actions.

Currently, these shares are quoting at Rs 45.30 and Rs 42.30 respectively (April 21, 2017). The aggregate value of the portfolio works out to Rs 18,872, a shade higher than the original cost of acquisition.

Global Broadcast News – another scorching launch

Now, Global Broadcast News Limited, another company promoted by the same group to offer general news in English, was off to a similar rousing start when it launched its IPO in January 2007. The shares, priced even higher at Rs 250 (a premium of Rs 240 per share over the face value of Rs 10), was oversubscribed 50 times. Yet today, the fate of investors in the shares of Global Broadcast News is perhaps even worse than that of their counterparts who subscribed to the shares in TEIL eight years earlier.

A stock split of 1:5 (reduction of face value from Rs 10 per share to Rs 2, thus converting a Rs 10 face value share into five Rs 2 face value shares) and renaming itself as TV 18 Broadcast Limited (TV 18) made investment in 100 shares now become 500 shares. But at the current market price of Rs 45.30 (April 21, 2017), the initial investment of Rs 25,000 is now worth only Rs 22,650 - roughly Rs 10 lower than the original cost of acquisition.

While Global Broadcast News as a broadcaster of general news in English did not have the early mover advantage of its sister company TEIL, which was a pioneer in business news broadcast in English, it did boast an impressive pedigree in being branded with CNN. Additionally, its operations were reinforced by the presence of a galaxy of media professionals experienced in television news broadcasting.

In the days to come, the fortunes of these two companies might yet be turned around. But that shouldn’t obscure the fact that, in the period between the time companies belonging to the Group raised money from the investing public for the first time, and now, there has been considerable destruction of investment value owing to a series of decisions taken by the management then in charge of the operations of the Group.

The promoters on their part paid the ultimate price by losing control of the Group as a consequence of decisions that they themselves took or willingly went along with.

How did it all go down in barely a decade?

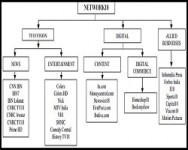

The Group started its corporate voyage as a company with one television channel broadcasting business and financial market news in English. It soon branched out into starting a similar channel, this time in Hindi. Along the way it saw value in setting up a general news channel and followed it up with an entertainment channel.

In no time at all, the Group had interests in 11 television channels focusing on different genres of programming, each with its own business rationale. It also founded or took over existing digital media assets that could build a relationship with potential customers which could later be monetised purely as a content platform or developed as an e-commerce portal.

Now, not all investments were financed out of shareholders’ money. A good chunk of it was funded out of borrowings. The burden of debt began to mount over time as the businesses in which investments that were already made, turned out to be losing propositions or needed fresh infusions of funds (which could be financed only out of further debt) before they could start to generate a profit.

With a business that was heavily laden with debt it was always a race against time between potentially good businesses starting to generate profits and the bad ones dragging the company’s operations down to a point of no return. Put differently, long before the good ones turned into money spigots the bad ones overwhelmed the company.

There soon came a point when Raghav Bahl had to find a saviour for the portfolio of businesses that had been put together, someone who not only saw value in some, if not all, but more importantly had the financial muscle to pay off the debts and turn around those that were viable by infusing even more funds into them.

The Group as a whole (consolidated balance sheet numbers) had outstanding loans to the tune of over Rs 1200 crore (Rs 1213.86, to be exact) as on March 31, 2012. Of this Rs 624.50 crore were repayable within the next 12 months, a sum that the Group’s operations could not generate on its own. Fatefully, Reliance Industries (RIL) was roped in, in 2012.

The early windfall income obscures the real picture

In the first financial year of operations as a listed company (October 99-September 00), TEIL posted a net profit of Rs 13.42 crore. But when you take into account the fact that the company was the beneficiary of windfall income that year which had nothing to do with the broadcast business, a discerning investor would have seen how difficult the operating environment was.

What happened was that the company had a huge pile of surplus cash (Rs 4,100 crore, roughly) that an overwhelming public response to the IPO had put in its coffers. The company’s annual report of that year coyly acknowledged the fact that it was the beneficiary of a one-time investment income that fetched it Rs 16 crore before the excess subscription money was eventually returned to unsuccessful investors.

(Of course, in later years, companies could not profit in such a fashion; the market regulator, SEBI, stepped in to make sure that the company could draw upon monies invested by the public only after the allotment process was completed and withdraw only so much of the money that they were allowed to raise in the first place through an IPO. Till then the money stayed in an investor’s bank account although it stood frozen till the company completed the allotment exercise.)

In TEIL’s case, if one took that windfall out of the equation, the operations that year were actually in the red. In other words, the business of broadcasting corporate and financial market news per se, did not generate any surplus that first year. The following year, which was a truncated one of six months (October 2000-March 2001), did see a surplus of Rs 3.18 crore without the cushion of any windfall income. This was further consolidated in the fiscal year April 2001- March 02 with the company turning in a net profit of Rs 3.43 crore.

But thereafter things began to take a turn for the worse in the two subsequent years (2002-03 and 2003-04), with the operations of the company registering losses of Rs 1.33 crore and Rs 3.93 crore, respectively.

The Mauritius connection

This was not all. Its Mauritian operation through which the programmes were beamed to an Indian audience - a structure that was imposed by the legal constraints of that time – was proving to be a drag on its bottomline. This became evident when the company hinted in its balance sheet as of March 31, 2003 that not all the monies due from its Mauritian subsidiary for sale of television programmes were recoverable.

It had estimated that as much as Rs 8.25 crore might not be recoverable, going forward. The accounts for that year also said that TEIL’s share of losses in the joint venture with CNBC, registered in Mauritius, was roughly Rs 9.16 crore.

It got worse in 2003-04. The company wrote off Rs 5.69 crore towards money due from its Mauritian subsidiary. Further, the company also claimed that its investments in the Mauritian subsidiary were now worth a lot less than what had been shown earlier, and consequently it was writing off Rs 40.75 crore from the value of its investment reckoned earlier.

To compound matters, the company also said that it was writing off Rs 13.68 crore out of the sums advanced as loans to the subsidiary. The three write-offs totalled Rs 60.12 crore.

The upshot of these adjustments, some of them directly reflected in the Profit and Loss Account and the rest adjusted against surplus in the Share Premium Account, was that they practically wiped out the money that had been collected from the public through the IPO in 1999.

If there were doubts back then that perhaps the profit reported in the two-year period 2000-02 may not really exist, then the disclosures and accounting adjustments of 2002-04 only served to reinforce such doubts. (Note: During the year ended 31 March, 2009, the Mauritian company eventually repaid the aforesaid loan and receivables amounting to Rs. 27.22 crore - USD 5.97 million - following its improved cash flows).

No doubt, the regulatory architecture prevailing then for transmitting of news by private players was partly to blame for the business structure, with an overseas intermediary being woven into the scheme of things, that TEIL was shown to have employed.

In the Government’s view, news broadcasting was a public sector monopoly under the Indian Telegraph Act 1885. While this was clearly anachronistic to the spirit of the post-liberalisation era of 1991, the liberalisation of the rules of engagement for private players in news broadcast took a long while to fructify. So players such as TEIL were resorting to novel ways of getting around the restriction.

A popular way of doing so was to transmit the content to an overseas subsidiary which in turn would beam the programme with or without co-branding involving a foreign broadcaster. The Indian company, after all, wasn’t doing anything illegal. It was producing news programmes and selling it to a foreign entity. That the foreign entity happened to be its own subsidiary was only incidental. Thereafter, what the foreign subsidiary was doing with the content was subject to local laws and Indian laws on broadcasting would clearly not apply to that process.

Now if it happens to tie up with another foreign company which providentially owns transponders on a satellite whose footprint happens to fall on the Indian land mass, surely the Indian company was not to be blamed? Or so the argument went.

In TEIL’s case, a Mauritian subsidiary (Television Eighteen Mauritius Limited or TEML) was created to purchase the transmitted programmes. TEML in turn teamed up with CNBC to beam these programmes to an audience that is largely resident in India. The resultant subscription income and advertising revenues were to be split up according to some pre-agreed formula.

A lot would therefore have depended on the joint venture between CNBC and TEML having a good infrastructure on the ground to enlist subscribers and to market the programmes to advertisers in India. The losses in the initial years would seem to suggest that this hadn’t been the case.

In March 2003, the Ministry of Information & Broadcasting (MIB) finally decided to open up the market for private news broadcasts by Indian companies. The uplinking guidelines, as they were called, did away with the need for an overseas subsidiary to handle the business end of things.

But the Mauritian subsidiary continued to cast its shadow on the operations for many years, and exists even to this date.

The impact of CNBC Awaaz

Also, TEIL had by now decided to add another string to its business bow. It had begun taking steps to launch a Hindi business news channel (CNBC Awaaz).

The channel went on air in January 2005, but it wouldn’t be until the second half of the fiscal 2006-07 that its operations got fully reflected in the finances of TEIL. There is some evidence to suggest that while the operations of the English business broadcast were stabilising, with profits in the two years 2004-05 and 2005-06 aggregating to Rs 39 crore, the operations of the Hindi business news channel were a financial drag.

In the first half of 2006-07, CNBC Awaaz suffered, roughly, a loss of Rs 6.5 crore. Against revenue of Rs 9.5 crore, the expenditure incurred amounted to Rs 16 crore. This was stated by the auditors of TEIL in their report to the shareholders of the company for the financial year 2006-07.

As if in further confirmation of this state of affairs, the profits before tax in that year (2006-07) halved to Rs 16.8 crore from Rs 31.65 crore in the previous year which had not been impacted by the operations of the Hindi channel. Indeed, the company told its shareholders that the Hindi channel on which it had invested close to Rs 55 crore had huge accumulated losses and consequently a good chunk of what had been shareholders’ monies invested in it had been wiped out.

So, while TEIL even as a standalone company (English business channel) was making profits in the years 2004-05 and 2005-06, there was no joy to be had from the operations of CNBC Awaaz. At least, not back then.

In fairness, it must be said that while the broadcast business was not exactly a ‘new economy’ in the sense of being akin to an IT or IT-enabled business, it was not a brick and mortar ‘old economy’ business either. Given the regulatory challenges and the need to establish a novelty such as a TV business news channel as a good advertising medium, a longish gestation period was only to be expected.

But that didn’t deter Raghav Bahl from setting his company on a course of such scorching pace that the turbulence of the initial years, such as they were, seemed in retrospect a period of peace and stability.

Though the government began to permit uplinking, the new rules of the business had a key condition: the promoters needed to ensure that they had more than 51% stake in the company before they could set about fulfilling their outsize ambitions. For Raghav Bahl, who had diluted his holdings to well below 51%, this was the first obstacle. How he got around it is a story in itself.

* The author is an editorial consultant with The Hindu Business Line.